Coinbase has identified over 20 instances where the Federal Deposit Insurance Corporation (FDIC) advised banks to refrain from engaging in crypto banking services, citing concerns related to consumer protection and financial stability.

Key Points

- The FDIC’s warnings to banks about crypto activities date back to March 2022.

- Coinbase’s findings include notable recommendations from FDIC officials urging banks to pause crypto initiatives.

- Coinbase is pursuing additional information regarding FDIC communications through FOIA requests.

Overview of FDIC Communications to Financial Institutions

Coinbase has uncovered more than 20 documented instances in which the Federal Deposit Insurance Corporation (FDIC) has advised banks in the United States to either pause or avoid engaging in cryptocurrency-related banking services.

This information, revealed through the Vaughn Index, sheds light on the regulatory approach of the FDIC towards cryptocurrency, highlighting ongoing concerns surrounding consumer protection, financial stability, and the operational integrity of banks involved in crypto transactions.

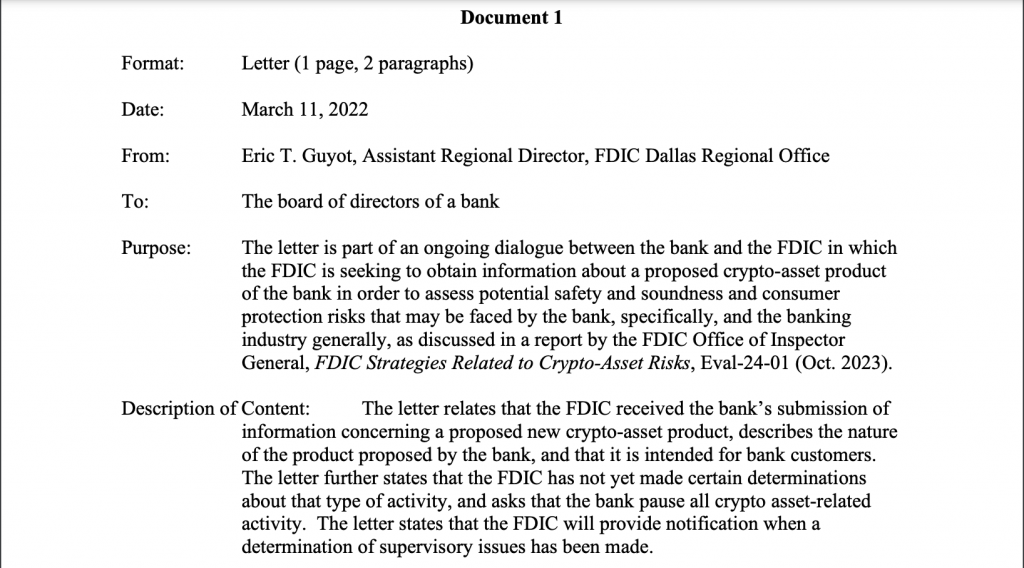

The documents reviewed by Coinbase include a series of letters and communications between the FDIC and various financial institutions. These correspondences suggest that as early as March 2022, the FDIC was expressing strong reservations about the potential risks posed by crypto assets, urging banks to halt related projects until supervisory concerns could be resolved.

For example, in a letter dated March 11, 2022, FDIC Assistant Regional Director Eric T. Guyot recommended that a particular bank “pause all crypto asset-related activity” while the agency evaluated the safety and soundness implications of the bank’s proposed crypto product.

Specific Instances of Regulatory Caution

Throughout the communications, several instances reflect the FDIC’s cautious approach. On March 25, 2022, FDIC Acting Regional Director Jessica A. Kaemingk advised a bank’s board of directors to reconsider its plans for a crypto-asset program due to concerns regarding “safety and soundness.” The FDIC requested additional documentation to ensure that the bank’s practices were in compliance with regulatory standards.

Later, on April 22, 2022, the FDIC requested that a bank pause its expansion of an existing cryptocurrency service. The agency sought further clarification regarding the bank’s compliance measures and risk management strategies before permitting any broader access to crypto services. Such communications point to a consistent regulatory stance aimed at preventing banks from entering the cryptocurrency market without adequate safeguards in place.

Implications for the Cryptocurrency Industry

Coinbase’s Chief Legal Officer, Paul Grewal, articulated concerns regarding the impact of the FDIC’s stances on the broader cryptocurrency industry. He emphasized that the documented communications reflect a troubling trend whereby a government agency is perceived to be limiting financial access for compliant American companies operating in the crypto space. In a recent post, he expressed that this situation serves as a “shameful example” of how regulatory actions can stifle innovation and access to essential banking services for legitimate businesses.

Grewal also highlighted Coinbase’s commitment to advocating for greater regulatory transparency. He stated that the company would continue to file Freedom of Information Act (FOIA) requests to uncover further details regarding the FDIC’s regulatory approach to cryptocurrencies.

“What we’ve seen so far speaks volumes; We’ll keep pushing to get clarity from our regulators through FOIA requests and any other means necessary.”

Paul Grewal, Coinbase’s Chief Legal Officer

This initiative aims to provide clarity for both financial institutions and crypto companies regarding the rules and expectations in the rapidly evolving landscape of digital assets.

Coinbase recently reported a significant drop in its stock value, which fell 15.3% following the release of third-quarter earnings that fell short of market expectations. The earnings report indicated a net income of $75 million, which did not meet the projected $112.2 million, and revealed a decrease in key performance metrics, including net revenue, which dropped from $1.38 billion in the previous quarter to $1.13 billion.

Despite the disappointing financial results, Coinbase announced a $1 billion share buyback program, reflecting its confidence in long-term prospects. Additionally, the company expressed optimism about the future of the cryptocurrency sector, particularly noting that major U.S. presidential candidates now hold favorable views toward cryptocurrency. In preparation for the 2026 midterm elections, Coinbase has committed an additional $25 million to support pro-crypto political candidates through the Fairshake PAC.

The FDIC’s warnings to banks regarding crypto-related services highlight significant regulatory concerns that may impact the future of cryptocurrency banking in the United States. As Coinbase continues to advocate for transparency and seeks further clarity on regulatory measures, the industry watches closely to gauge the potential effects of these developments on both financial institutions and the broader cryptocurrency market.

Disclaimer: All information provided on this website is for informational purposes only and should not be construed as financial or investment advice. We do not guarantee the accuracy, completeness, or timeliness of the information, and we are not responsible for any financial decisions you may make based on this information. Cryptocurrencies are highly volatile assets, and any investment in them carries a high level of risk.

More Like This

Ark Invest Sells $3.9 Million In Coinbase Shares

HBAR May Get ETF Approval Before Solana or XRP Does

*AI technology may have been used to develop this story and publish it as quickly as possible.